The gaining traction of electric vehicles (EV) industry and the renewable energy adoption of Europe have been pushing the local demand higher. However, the lack of native supply has allowed many international Asian companies such as LG Chem and Samsung to take over the market. In fact, in 2018, less than 3% of total demand was supplied by European companies for the EV market. The domination increases as far east continue to invest steeply in local production sites and production ramp-ups, however, early investment and generous market share consolidation are priceless. Also, the investment is more than welcome for the EU and especially Germany, as the leading country of preference, the companies may skip transportation costs, import/export taxation due to EU regulations and might even dodge the recently implemented importation quotas of U.S. in the meantime when the origin of the goods is Europe. But why we still don’t have globally competing battery manufacturers in Europe if there is massive demand, change of politics, and policies that enable production?

Why Academia and Not Industry?

This is the type of question a doctoral candidate might have in his/her mind whether to continue in academia or switch to industry. Still, it also reflects the existence of internationally-known, fine European institutions with vast R&D possibilities, innovation, and technology on batteries but no industrial entrepreneurship for production. R&D, innovation, and technology are not just buzz words in Europe, but they truly exist. So why this know-how has not already acted on in the industry? Why has Europe been lagging in battery production? What might have been lacking so far was the feasibility of the produced technology versus price. So far, in Asian countries, and especially in China, there has not been a working-class movement to uphold the effective regulations and well-being of people due to the political climate.

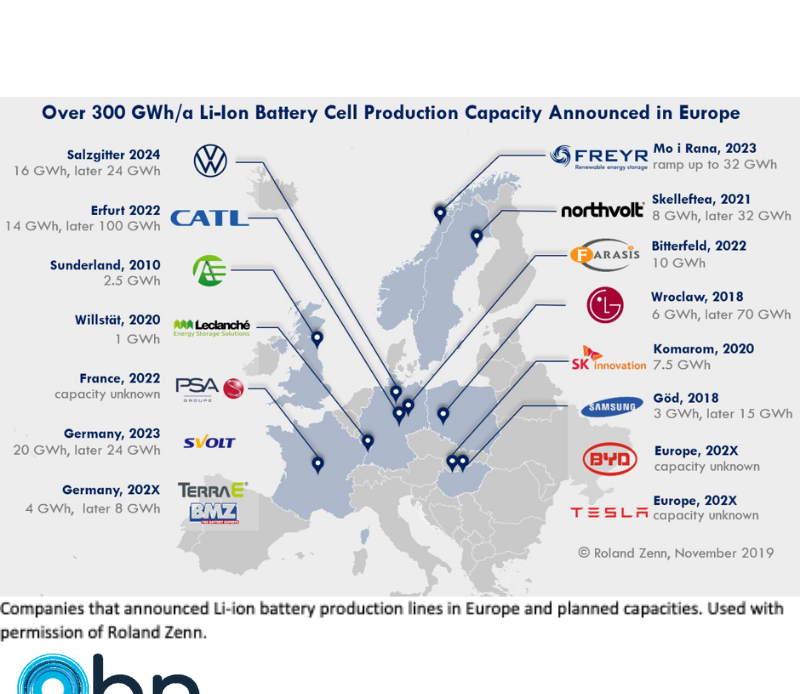

In contrast, Europe has strict regulations for the workplace, has guilds and safety guidelines, and hourly labor is expensive compared to their Asian counterparts even when compared to East European countries. Also, the working and earning culture has a broad impact on investment decisions, where margin earnings through immense mass production are the standard in the far east in comparison to Europe’s more tailored, thought-through investment system with higher earning expectancy than just numbers of revenue. Until now, the earning feasibility to production quality parity did not have a good ratio for Europeans. The recent technological developments, record-breaking demand for batteries on many fronts, and even a bit of fear-of-missing-out may have encouraged the European investors and institutions to act and unite. This includes a strategic formation of European Commission, EU countries, European Investment Bank, industrial stakeholders and innovation under the name of European Battery Alliance in 2017 as well as European Portable Battery Association (EPBA), a regulatory association that bridges companies, consumers and authorities, and EUROBAT for automotive and industrial battery manufacturers. Now, in addition to Asia-based international players in Europe such as CATL, BYD, SVolt from China, Envision AESC from Japan, SK Innovation, LG Chem, Samsung from South Korea and Freyr Energy from India producing a total of around 250 GWh, there will be at least a couple of European producers like French PSA group, German Volkswagen and Terrae-BMZ and Swedish Northvolt. However, their announced plans of production still only mount to 64 GWh with ramped up production numbers (unknown capacity of PSA group). The market will be at its most competitive state past mid-20s, also with the arrival of some US-based companies like Farasis and Tesla-Panasonic, which very recently announced will be building Gigafactory 4 close to Berlin, Germany. But the good news is, the industrial spirit of Europe shows signs of revival, to fight its place for the local market, if not for the global one. Under all these circumstances, a politically and economically stable Turkey would become the perfect ally for the Europeans, providing competitive labor pricing, a large dynamic workforce with high efficiency, and innovative drive.

References:

Image credits: http://linkedin.com/in/roland-zenn

https://ec.europa.eu/growth/industry/policy/european-battery-alliance_en

https://www.eurobat.org/about-eurobat

https://electrek.co/2019/11/12/tesla-gigafactory-4-berlin-germany/